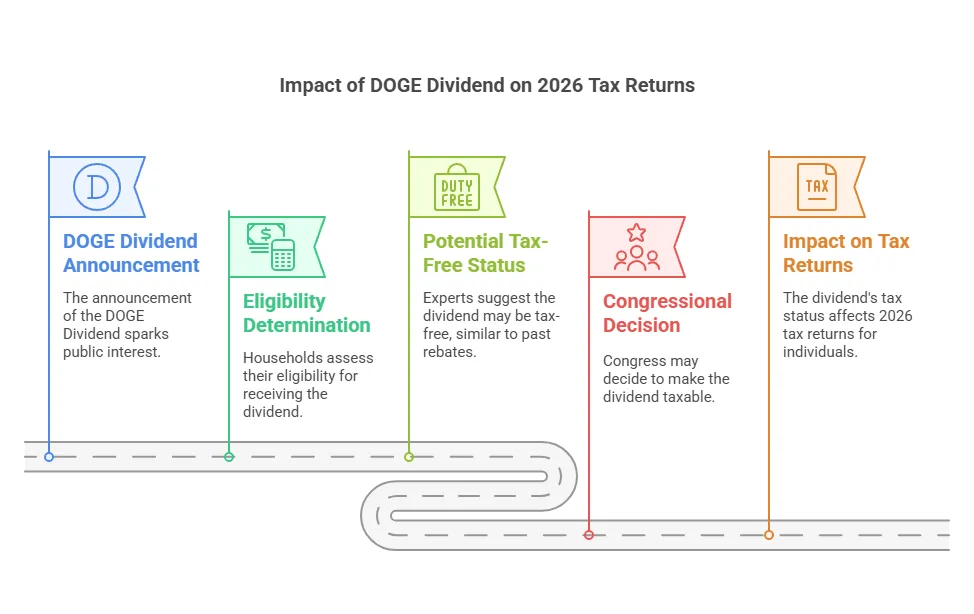

DOGE Dividend tax impact 2026: The DOGE Dividend—a proposed payout from President Donald Trump and Elon Musk—promises to send cash back to taxpayers by July 2026. Fueled by savings from the Department of Government Efficiency (DOGE), this plan could mean $5,000 checks for millions. But what does it do to your taxes? This article digs into the tax impact of the DOGE Dividend in 2026, breaking down eligibility, taxability, and planning steps you can take now.

- Trump Largest Social Security Tax Cut 2025: The Largest Social Security Tax Cut in History?

- Child Tax Credit for 2025: Maximize Your Refund!

- Shocking Post-Election Market Trends Every Investor Must Know!

- Scandal Alert: The Real Reason Behind the Senate-House Split Over Trump Tax Cuts!

Will the DOGE Dividend Hit Your Tax Bill?

The DOGE Dividend could alter your 2026 tax return. Experts estimate 79 million households might qualify as “net payers of federal income tax.” That’s the group likely to see a check. If you pay no federal income tax in 2025—say, because of credits or low income—you probably won’t get it. The payout itself might not count as taxable income. Past rebates, like the 2020 stimulus checks, dodged taxes. Posts on X from investment manager James Fishback suggest this dividend aims to follow suit. A tax-free $5,000 lands in your pocket without pushing you into a higher bracket. But if Congress tweaks it—like making it taxable—your 2026 tax bill could climb. Picture earning $50,000 in 2026. A taxable $5,000 bumps your income to $55,000, adding a few hundred bucks to your taxes.

This was exciting to hear $5000 DOGE Dividend at first, but to qualify you have to be a 'net payer of federal income tax'. That means…federal income tax is sticking around folks. At least through 2026… https://t.co/EhrPo6emO1

— Jin Cuts (@jincuts843) February 19, 2025

Key Dates and Details for the DOGE Dividend

| Event/Data Point | Details |

|---|---|

| Proposal Announced | February 19, 2025 |

| DOGE Program Start | Assumed active as of early 2025 |

| DOGE Program End | July 2026—planned expiration date |

| Dividend Distribution | Expected July 2026, post-DOGE savings calculation |

| Estimated Households | 79 million “net payers” (per James Fishback) |

| Proposed Payout | $5,000 per eligible household |

| Savings Goal | $2 trillion by July 2026 (official DOGE target) |

| Current Savings Claim | $55 billion as of February 2025 (unverified) |

| Tax Status | Likely non-taxable, pending Congressional approval |

| Official Source | No dedicated site yet; track updates at whitehouse.gov |

Who Gets the DOGE Dividend?

Eligibility ties straight to your tax status. You need to owe federal income tax in 2025 after credits. Earn $30,000 but claim a $3,000 Earned Income Tax Credit? If your tax owed drops to zero, you’re out. Fishback says this targets “net payers” to reward workers. That could push some people—like retirees or part-timers—to take jobs in 2025. More income then might mean a bigger 2026 tax hit. Say you pick up a $20,000 gig to qualify. Your 2026 return could reflect that extra cash, raising what you owe. Check your 2024 return now. It’s a clue to whether you’ll need to adjust.

Can You Plan Ahead for the Tax Impact?

Yes, you can act now. If the dividend stays tax-free, it won’t mess with credits like the Child Tax Credit in 2026. But if your income jumps to qualify, plan for the ripple. Boost your 401(k) contributions in 2025. That cuts your taxable income later. Got $5,000 extra from the dividend? Stash it in an IRA by April 2027. It trims your 2026 tax load. Ask yourself: does your current tax setup make you a “net payer”? If not, small moves—like picking up freelance work—could lock in your spot.

DOGE Dividend Savings Scenarios

| Savings Achieved | Payout Per Household | Tax Impact (If Taxable) |

|---|---|---|

| $2 trillion | $5,000 | $750 more tax (15% bracket) |

| $1 trillion | $2,500 | $375 more tax (15% bracket) |

| $500 billion | $1,250 | $187 more tax (15% bracket) |

| $250 billion | $625 | $94 more tax (15% bracket) |

| $100 billion | $250 | $37 more tax (15% bracket) |

| $55 billion | $138 | $20 more tax (15% bracket) |

| $2 trillion | $5,000 | $0 (if non-taxable) |

| $1 trillion | $2,500 | $0 (if non-taxable) |

| $500 billion | $1,250 | $0 (if non-taxable) |

| $55 billion | $138 | $0 (if non-taxable) |

Does the DOGE Dividend Change Your Job Plans?

Fishback claims it might pull people into work. Want that $5,000? You need taxable income in 2025. A stay-at-home parent might grab a part-time job. That boosts your 2025 earnings—and your 2026 taxes. Look at Jane, a hypothetical freelancer. She earns $10,000 now but takes a $15,000 job in 2025 to qualify. Her 2026 tax bill rises by $2,250 (15% rate). The $5,000 payout offsets it, leaving her ahead. Think about your situation. Could a small gig tip the scales?

Timing Matters for Your 2026 Return

The payout hits in July 2026. That’s after your 2025 return (filed April 2026). Any tax impact—good or bad—lands on your 2026 return, filed in 2027. Trump’s broader tax plans might shift rates by then. A lower rate could soften a taxable dividend’s sting. Higher rates? You’d feel it more. Start tracking DOGE savings now. If it falls short of $2 trillion—like the $55 billion claimed today—your check shrinks. A $1,250 payout still helps, but tax planning gets trickier.

The DOGE Dividend tax impact in 2026 hinges on final rules. A tax-free $5,000 boosts your cash with no catch. A taxable payout—or extra work to qualify—shifts your numbers. Check your tax status today. Adjust your income or savings plans. You’ll be ready either way.

- Reasons to Choose Megapari for Sports Betting in India

- June 2025 Visa Bulletin Breakdown: No Progress for EB-1, EB-2 – What Now?

- $1500 Stimulus Checks 2025: Are You Eligible? Apply Now!

- $2000 Senior Stimulus Payment: Eligibility, Timing, & Resources

- Are You Getting a $1500 Stimulus Check in 2024? Here’s How to Find Out

FAQ Related To DOGE Dividend tax impact 2026

Probably not. It’s pitched as a tax-free refund, like 2020 stimulus checks. Congress could change that, so watch updates.

You need to owe federal income tax in 2025 after credits. File a return showing “net payer” status to check.

July 2026 payout means it hits your 2026 return, filed in 2027. Plan ahead for that year.

Join WhatsApp

Join WhatsApp

Join Telegram

Join Telegram